Internal energy market and renewable energy sources

22. Máj, 2013, Autor článku: Beláň Anton, Elektrotechnika

Ročník 6, číslo 5  Pridať príspevok

Pridať príspevok

![]() The varied character of the European Union´s electricity market has given rise to a number of the issues for the energy sector, consumers and for the future competitiveness of the European Union as a whole. In many Member States there is not enough competition in the electricity market level neither in industry level. Lack of the competition has led to a dearth of innovations, based on the creation of an internal market for energy has become one of the main objectives of the priority of the European Union. This article deals with the current challenges in the field of the internal energy market in relation to renewable energy sources.

The varied character of the European Union´s electricity market has given rise to a number of the issues for the energy sector, consumers and for the future competitiveness of the European Union as a whole. In many Member States there is not enough competition in the electricity market level neither in industry level. Lack of the competition has led to a dearth of innovations, based on the creation of an internal market for energy has become one of the main objectives of the priority of the European Union. This article deals with the current challenges in the field of the internal energy market in relation to renewable energy sources.

Introduction

For the European Union in the framework of further progress in the energy sector is necessary a competitive and integrated internal energy market providing electricity flowing where it is needed. To tackle Europe´s energy and climate challenges and to ensure affordable and secure energy supplies to households and businesses, the European Union must ensure that the internal European energy market is able to operate efficiently and flexibly. Despite major advances in recent years in the way the energy market works, more must be done to integrate markets, improve competition and respond to new challenges. Accordingly the European Governments set a deadline of year 2014 for completion of the internal energy market. The internal energy market is not an end in itself. It is a key instrument in delivering economic growth, jobs, secure coverage of their basic needs at an affordable and competitive price, and sustainable use of limited resources.

1. Present and future challenges of integrated energy market

By 2014 it is necessary to implement and enforce the existing legislation fully, including the establishment of basic technical rules at the European Union level and provide to regulatory authorities the necessary tools to effectively use of laws. Cross – border electricity markets must be up in all parts of the European Union and the implementation of plans to complete and modernize European networks must be well under way. Only when this is achieved, customers will reap benefits of the internal energy market. Today, the deadline is almost unrealizable. Member States do not comply the deadlines to adjust their national legislation and create a competitive market with consumer participation. Nevertheless it is seeing the progress of Member States to meeting the common objective and creating efficient and secure energy systems transcending national borders.

1.1 The benefits of integrated energy market

National governments, large corporations and individuals must be convinced that the internal energy market is the best choice. This is not true at the moment. The current markets are still highly concentrated. In eight Member States more than 80 % of the power generation is still controlled by the historic monopoly. In a well functioning electricity market the investments should be driven by market instead of subsidies. Energy markets are generally perceived as transparent and open enough for newcomers in the market. Economically rational investments in energy efficiency are not being made – or at least not enough. Consumer satisfaction is low even in Member States that today have fairly competitive energy markets.

1.2 Partial results of integrated energy markets

In present is possible to see some of the benefits and results of integrated energy market in particular by improving the conditions for electricity consumers and have a positive impact on electricity prices:

- More choice for electricity consumers – at least 14 European electricity companies are now active in more than one Member State and there are more than three main electricity suppliers in twenty Member States [1]. Households and small businesses in two third of the Member States can choose their electricity supplier. Consumers can compare and choose the best deal.

- More competitive pricing – new energy legislation which heads promote competitive conditions allow the market opening, increasing cross – border trade, market integration and contributed to more intense competition and the maintenance of energy prices. Consumer’s payment for energy consists of several elements, what can be confusing. They are all determined at Member States level and subject to national policies [2]. In some Member States taxes and levies constitute around 50 % of final energy bill [2]. In the EU – 15, taxes in the final bill for domestic customers increased on average from 22 % in 1998 to 28 % in 2010 [3].

- More liquid and transparent wholesale markets – transparency in traded electricity markets have gradually improved as the result of market coupling between Member States [2]. Market coupling has spread steadily from the North – West of the European Union to other regions. At present, 17 Member States are coupled

- More secure suppliers – higher liquidity of wholesale markets increased the secure of energy supply in the European Union

- The European Union and Member States have recognized that is need to improve cooperation with third countries. This give the European Union more weight in energy related trade relations.

1.3 Possible improvements in the future

Besides the above mentioned advantages and improvements in the future we can expect further changes that will be perceived positively:

- More power for consumers to control their energy costs – it is clear that the energy prices will continue to increase due to the increased demand for fuel and also due to the modernization of the energy system [4]. However, the integrated energy market ensures that household spending will not be subject to competitive pressure from suppliers. Estimates indicate that already today European Union consumers could save up to 13 billion Euros per year if they switched to the cheapest electricity tariff available [2].

- Better control of consumption through smart technologies – further technical development will support the trend of smart technology. Smart technology can help reduce household energy consumption. In addition smart technology allows adjustment of electricity consumption n real time in response to fluctuations in market prices.

- More efficient use a development of grids – pan – European technical regulations may give further improvement of efficiency of the network. New technical regulations with combination with smart grid can help improve system flexibility and extensive integration of renewable energy sources. This will enable renewable energy producers to participate fully in a truly competitive market and progressively take on the same responsibilities as conventional generators, including as regards balancing

2. Global potential of solar energy sources

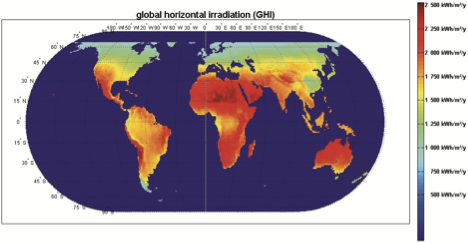

Energy source availability is decisive for all power technologies. The basis for all solar energy technologies is the amount and the composition of the global horizontal irradiation (GHI). Different solar system concepts have been developed for optimizing the energy yield. Solar resources adapted to system requirements are derived and compared with each other. Global horizontal irradiation is more or less homogenously distributed on Earth (Figure 1).

Fig. 1 Annual global horizontal irradiation (GHI) [5]

Variations of GHI for most populated regions in the world are typically within a range of a factor of two, e.g. Central Europe (~ 1 100 kWh/m2/y) and Arabian Peninsula (~ 2 200 kWh/m2/y). Absolute and relative diffuse radiation depends on regional climatic conditions, especially with the presence of clouds. Diffuse irradiation is lost for solar power technologies only capable of converting direct solar irradiation, thus sites of low diffuse irradiation are most appropriate for these technologies.

A major advantage of photovoltaic (PV) technology is the need for no moving parts. 1-axis north-south horizontal continuous tracking systems follow the Sun over the day. 1-axis north-south optimally tilted tracking systems are better adapted to each site latitude. The PV system of highest annual irradiation is the 2-axes non-concentrating tracking system. A large plant area is needed due to two directional shading effects and a higher mechanical stress and cost is effective due to more moving parts and engines. 2-axes concentrating tracking variation are only needed for high concentrating PV (HCPV) systems and solar thermal electricity generation (STEG) [5].

Summarizing the results, 1-axis horizontal north-south continuous tracking PV systems might be competitive for fixed optimally tilted PV systems. An increase in irradiation of 20–30 % for sunny and very sunny regions might justify higher capital and operational expenditures, especially for plant operators achieving further advantages by more full load hours of the PV plant [6]. 2-axes non-concentrating and concentrating tracking PV systems further increase the irradiation on the module surface, however the higher complexity of such systems significantly reduces the financial benefits of these approaches.

In the case of HCPV systems, significantly higher power conversion efficiencies in reference to nonconcentrating PV systems result in about 35 % higher electricity generation potential per area unit, leading to a beneficial cost potential of HCPV systems. In total, solar resource is available in all populated regions in the world. Fixed optimally tilted PV systems are the standard PV power plant system types, however depending on local conditions, adapted tracking systems increase the annual yield per installed capacity and lower the power generation cost.

2.1 PV market potential for 2020

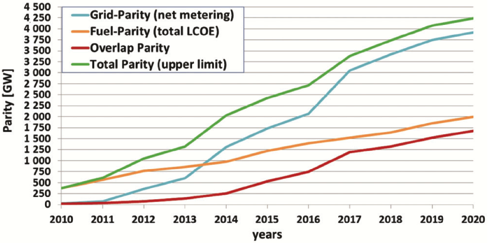

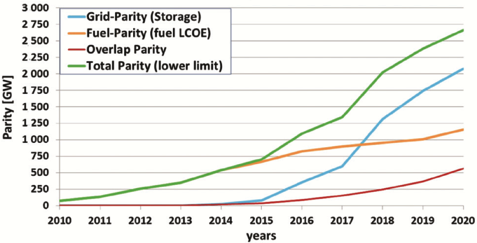

Photovoltaic energy technology has the potential to contribute to the global energy supply on a large scale. This potential can only be realized if sustainable and highly competitive PV economics are achieved. An integrated economic PV market potential assessment is presented consisting of grid-parity and fuel-parity analyses for the on-grid markets and an amortization analysis for rural off-grid PV markets. All analyses are mainly driven by cost projections based on the experience curve approach and growth rates for PV systems and electricity and fossil fuel prices for the currently used power supply. Finally the outcome of the derived economic PV market potential has been transformed to pessimistic, realistic and optimistic estimates of a cumulated installed PV capacity by the end of 2020. These installed capacity estimates are compared with PV scenarios published by leading organizations in the field of energy and PV scenarios [5].

The economic PV market potential derived by the gridparity approach is estimated to about 980 GW up to 3 930 GW and in the most likely case to about 2 070 GW by the year 2020, if an advanced economic storage system for PV electricity is available [7]. The market estimate according to the fuel-parity approach leads to about 900 GW up to 1 500 GW fully economic potential for PV power plants in the year 2020 [7]. The total addressable economic market potential for rural off-grid PV applications is estimated as about 70 GW [7]. An integrated economic PV market potential has been performed to avoid double counting. The integrated assessment leads to an overall sustainable economic PV market potential of about 2 800 GW to 4 300 GW in the year 2020 [7].

The outcome is depicted in Figure 2 for an integrated sustainable economic market potential estimate for PV systems on the basis of a learning rate of 20 % for modules and inverters and 15 % for the other balance of system (BOS) components. Only a fraction of the market potential will be realized in time, thus PV market expectations are derived resulting in cumulated installed PV capacity for the year 2020 in a pessimistic (600 GW installed capacity in 2020 and an annual growth rate of 20 %), realistic (1 000 GW in 2020 and growth rate of 30 %) and optimistic market view (1 600 GW in 2020 and growth rate of 40 percent) [7]. Only EPIA and Greenpeace can imagine such a fast progress in PV development. Other leading organizations like the IEA, WWF and EWG expect about one third or even less compared with the derived pessimistic market expectation.

Due to the complementarity of solar PV and wind power, market expectations for PV need not be lowered. Moreover, being complementary to wind power, PV together with wind power might become the backbone of the global energy supply in the coming decades [8,9]. However, hybrid PV-Wind systems are very likely to start to strongly influence the global power system in the next decade by sophisticated hybrid concepts, like renewable power methane technology. The fast progress of sustainable energy technologies seems not to be included in current energy scenarios of leading international organizations. Plenty of indications are given that several organizations would make no mistake in revising their scenarios in the field of PV. In conclusion, PV is on its way to become a highly competitive energy technology.

Fig. 2 Total economic market potential for PV systems in the upper (top) and lower limit (bottom) [5].

Conclusion

Market opening gives consumers a choice. There are still many problems that need to be urgently solved in order to complete the internal energy market by 2014. The European Commission is committed to providing and address the challenges associated with building and modernization of energy networks and the integration of renewable energy sources though a stable regulatory framework that sets out the tasks of all subjects in the electricity market.

Acknowledgements

References

- European Commission, Staff Working Document entitled Energy Markets in the European Union in 2011, referred to as “SWD 1″, [online]. November 2012. [cit. 27.6.2013]. Available on:

http://ec.europa.eu/energy/gas_electricity/doc/20121217_ energy_market_2011_lr_en.pdf - European Commission, Communication from the commission to the European Parliament, the Council, the European economic and Social Committee and the Committee of the regions: Making the internal energy market work, [online]. November 2012. [cit. 27.6.2013]. Available on:

http://ec.europa.eu/energy/gaselectricity/doc /20121217energy_market_2011_lr_en.pdf - Price developments on the EU retail markets for electricity and gas 1998 – 2011, page 2 [online]. [cit. 27.6.2013]. Available on:

http://ec.europa.eu/energy/observatory/ electricity/doc/analysis_retail.pdf - European Commission, Commission’s Communication “Energy Roadmap 2050″, pages 2, 5, 6 and 7. [online]. December 2012. [cit. 27.6.2013]. Available on:

http://ec.europa.eu/energy/energy2020/roadmap/doc/roadmap2050_ia_20120430_en.pdf - KOMOTO, K., BREYER, C., CUNOW, E., MEGHERBI, K., FAIMAN, K., VLEUTEN, P., Energy from the desert: Very Large Scale Photovoltaic Power – State of the Art and Into the Future. 2013. 2 Park Square, Milton Park, Abingdon, Oxon. ISBN13: 978-0-415-63982-8

- KOMOTO, K., ITO, M., VLEUTEN, P., FAIMAN, D., KUROKAWA, K., Energy from the Desert: Very Large Scale Photovoltaic Systems: Socio-economic, Financial, Technical and Environmental Aspects. 2007. Routledge. ISBN: 978-1844077946

- BREYER CH. The Photovoltaic Reality Ahead: Terawatt Scale Market Potential Powered by Pico to Gigawatt PV Systems and Enabled by High Learning and Growth Rates. 2011. 26th EU PVSEC, Hamburg, DOI: 10.4229/26thEUPVSEC2011-6EP.1.2.

- GERLACH A.-K., STETTER D., SCHMID J., BREYER CH., PV and Wind Power Complementary Technologies. 2011. 26th EU PVSEC, Hamburg, September 5–9.

- BREYER CH., RIEKE S., STERNER M., SCHMID J. Hybrid PV-Wind-Renewable Methane Power Plants – A Potential Cornerstone of Global Energy Supply. 2011. 26th EU PVSEC, Hamburg, September 5–9.

Co author of this paper are Dominik Viglaš, Boris Cintula, Pavol Heretík, Matúš Kováč, Vladimír Volčko, Anton Cerman, Institute of Power and Applied Electrical Engineering, Department of Electrical Power Engineering, Ikovičova 3, 812 19 Bratislava 1