Methods for detection of insurance fraud in motor vehicles

20. August, 2014, Autor článku: Chrobák Pavel, Informačné technológie

Ročník 7, číslo 8  Pridať príspevok

Pridať príspevok

![]() The paper deals with the investigation of insurance fraud in connection with the insurance of motor vehicles. In the introductory section describes the basic characteristics and methods of committing the crime of insurance fraud. The next part deals with motor vehicle insurance fraud, which in recent years there has been a large increase. In the last part of the paper gives specific case of detected insurance fraud.

The paper deals with the investigation of insurance fraud in connection with the insurance of motor vehicles. In the introductory section describes the basic characteristics and methods of committing the crime of insurance fraud. The next part deals with motor vehicle insurance fraud, which in recent years there has been a large increase. In the last part of the paper gives specific case of detected insurance fraud.

Introduction

The human society since time immemorial is constantly threatened by fears of unexpected events, originating from both natural processes in nature, as well as imperfections in the company itself. The basic feature of these harmful events is their randomness in time and extent of the consequences. Thus arose insurance that provides citizens the right to payment of funds to cover the needs arising from these incidents. The idea of the principle of insurance is very old already around 2000 B.C conclude caravan owners in Babylonia agreement on mutual protection of losses. With the gradual development of this new industry also began to appear first attempts at unauthorized obtaining compensation for loss of goods.

Basic characteristics and methods of committing insurance fraud

Fraud is one of the types of crimes that belong to the category of property crime and is considered a very dangerous form of crime, especially for qualification and occurrence, both in terms of general crime and economic crime in the area [5,7,8]. Insurance fraud can be generally characterized as deliberate (intentional) deception of one party to another for the purpose of obtaining or providing advantage to which they would not if it were true explanation of the facts. Misleading conduct may apply to any stage of the insurance contract, which in practice may mean that the damage (the insured event) is happened, did not in the manner or does not fall under the insured risk or it does not damage, injury or loss. In the event that the event actually occurred, so the fraud can occur that damage includes for example.

Undamaged parts of vehicles or other objects, the amount is exaggerated intentionally for this purpose that the resulting injury, damage or loss is covered by insurance (particularly in the case of co-insurance) or above is deliberately exaggerated in order to increase the value of the damage. It can be said that the insured event is fraudulent, even if fraudulent conduct applies only to the portion of the premiums. On the contrary, error, unintentional bias or lack of care can not qualify as a fraud, because the act or omission does not intent to deceive. The basic difference between these two terms, then, is that the condition of completion of the crime of fraud is to enrich the offender or another person. Whereas with insurance fraud is not necessary to completion of the crime for the damage, both pecuniary and non-pecuniary nature as well as possibly. In terms of forensic methodology can elaborate insurance fraud in several ways, misrepresentation or use of mistake in fact activities or events for pension insurance, accident insurance, hospitals expenses, building insurance, travel insurance, etc.

Division of Insurance Fraud attack by subject

Insurance Fraud divided by the subject of attack for claims arising under life insurance (personal insurance) or non-life insurance (property and liability insurance for damage) that can still divide by way of insurance statutory or contractual. Insurance claim in relation to life insurance arise in the pension insurance, accident insurance, medical expenses insurance, income insurance in sick leave, insurance serious diseases [2, 7]. Insurance events arise in relation to non-life insurance within household insurance including holiday homes, buildings insurance, travel insurance, accident insurance, motor vehicle insurance for damage caused by a motor vehicle liability insurance, liability insurance of the professional, industrial and business insurance, credit insurance [2, 7].

Distribution of insurance fraud by a person of the offender

In addition to distribution according to the subject of attack can be insurance fraud divide according to person the offender to external and internal insurance fraud. The external insurance fraud perpetrator is insured or policyholder, ie. Person whose property is insured or a person who has entered into with an insurer (insurance company) insurance contract. These offenders usually do not have any accomplices among the staff of the undertaking [1,3,7]. Offenders are mislead an insurance company or use error in fact or business events in negotiating an insurance contract or enforce a claim arising out of this contract, thus committing the fraud.

For internal insurance fraud perpetrator is an employee insurance, which is not usually as accomplices of the insured or the policyholder. Offender misrepresentation or mistake in fact use activities or events, make use of the well-known insurance business and in negotiating an insurance contract or enforce a claim stemming from the insurance policy far better use of various imperfections of the insurance product. They do not therefore fraudulent conduct in the true sense of the word, but their behavior is closer to meeting a similar fraud. Legal qualification of such negotiations depends on the way the offender committing a [1,3,7].

Insurance fraud in motor vehicles

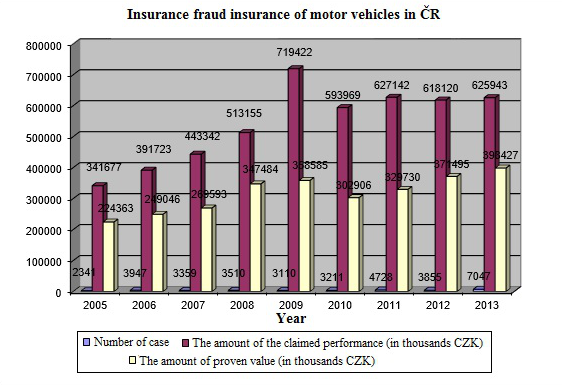

The economic situation in recent years has caused a number of subjects in both the private and business sector in a significant loss of revenue, which was then one of them decided to compensate for the expense of insurance companies. Number of attempts insurance fraud lately constantly grows and begins to grow in the international dimension, particularly with regard to the possibilities of free movement of persons and goods, barrier-free insurance risks within the EU and increasing professionalization of organized crime. According to estimates, the world is in selected segments of the insurance, especially in the case of cars, up to 30% of claims associated with insurance fraud. Last educated guesses then report overall average of 10% of undetected insurance fraud claims paid on a European scale [8,9]. In 2013 it was in Czech Republic by Czech Insurance Association (ČAP) examined over 10,000 claims and evidence of insurance fraud worth more than CZK 1 billion, of which about 40% of cases fall within the motor insurance segment as shown in the following figure 1.

Fig.1 Insurance fraud insurance of motor vehicles [9]

The increase in the number of cases investigated, accompanied by an increase in proven value, is still effective investigative methods and the use of modern technology. Insurance companies are also more focused on the detection of fraud related to bodily injury, which are applied by liability insurance. This damage often have high amounts of insurance claims. The fight against insurance fraud is not essential for society because undetected insurance fraud leads to deterioration of the general insurance claims ratio with a direct impact on the amount of premiums of all honest clients. Generally, insurance fraud related to motor vehicles mostly with accident insurance and third party liability. Accident insurance is most often attempted fraud during transport accident caused by the driver of the vehicle claiming more damage than actually occurred, or it is a fake cases of theft or damage clean vehicles.

Car insurance fraud occurs mainly in cooperation with members of the traffic police make fake reports of a traffic accident, then insurance professionals to explore the docks another crashed vehicle, or lower damage, which is not required examination of a crashed car insurance company employee, report the alleged incident, showing confirmation from the police and claim they keep liquidate insurance budget. Perpetrators often the participation of the second driver, usually your friend, staging alleged traffic accident that after leaving the police to investigate and damage to the vehicle covered by the insurer in respect of insurance of a “known” or in collaboration with the staff of car repair intentionally overestimate the cost of repairs.

Suggestions for investigation

Suggestions for the investigation of crimes of insurance fraud are either the injured party (the insurer) or the results of operatively-search activity. Announcements of the insurer. Notification of suspected that the crime was committed insurance fraud serves representative of the insurer, which has been applied to an insurance claim arising from insurance contracts previously concluded [2,4,5,6]. This notification is submitted by insurers after taking the examination received reporting a claim found circumstances that suggest that either the insured event did not occur, or event referred to as the insurance was another in a way that was not based claim. In the context of the notification forwarded to the insurer’s representative bodies active in criminal proceedings generally complex material revealing of insurance and the claim for indemnification including the knowledge gained the examination.

A typical example of such a notice is insured event that happened a few years ago at one of the large insurance companies in the country. Client (damaged) reported operator insurance claim for a car accident along with all necessary information for disposal see. Table 1 and described her course of an accident that occurred.

Table 1: Information about car accident

| Information about car accident | |

| 1 | When and where the traffic accident occurred |

| 2 | Who caused a traffic accident |

| 3 | Policy number |

| 4 | Data on damaged |

| 5 | Details of vehicle damage |

| 6 | The extent of damage to the vehicle |

| 7 | The estimated amount of damage |

| 8 | Polis road accident |

| 9 | Witnesses |

Kia Rio the vehicle was parked in a row of parked vehicles, which caught the truck driver T. Iveco Daily at the entrance to the passage electrical outlets. In doing damage to a parked car Kia Rio left-side mirror, paint and protective strips on the doors. During this maneuver the truck driver could not go into the passage electrical outlets because he to luggage lampposts, which is close to the entrance to the sidewalk. When he found out that not ride truck in transit, decided to back off a bit and reversing hit the left rear of the truck Iveco Daily T. again in the Kia Rio. When the collision occurred on the vehicle Kia Rio for damage to the left front, the destruction of breaking the bumper and left headlight and hood damage. After this his failed attempt to go to outlets passage was already stopped the owner of the parked vehicle [7].

The next day liquidation department reported an accident insurance culprit. Operator wanted by the driver of a truck Iveco Daily T. know the following details see. Table 1 together with a description of his version of a traffic accident. The driver said that he wanted his truck Iveco Daily T. electrical outlets go into the passage. Thus came closer to a number of stationary vehicles in order to enter the passage in the notice that caught the rear of a parked Kia Rio. In the entrance he did not go because he to luggage lamp post. He decided to back off a little and it went off when reversing foot from the clutch. The truck suddenly pulled away and crashed into the rear of a parked passenger car Kia Rio. This impact can already noticed, and soon it appeared to him the owner of a parked vehicle. When he got out of the truck found that the vehicle is parked Kia Rio damaged left mirror, paint on the doors and hood along with light [7].

Solution insured event

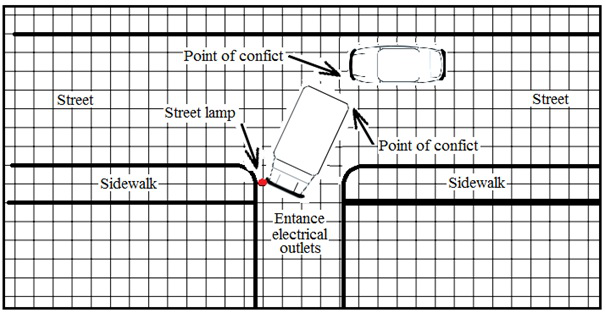

After reporting a traffic accident culprit also damaged the insurance company gave the operator all the information along with a diagram during a traffic accident in Figure 2 liquidator claims.

Fig.2 Drawing during a traffic accident [7]

The liquidator is based on evaluation of two telephone recording and drawing during a traffic accident became interested in the wrecked vehicle and agreed with the inspection of the damaged car Kia Rio to appreciate the damage caused to the vehicle. During inspection of the damaged car Kia Rio in Figure 3, the liquidator concluded that the accident did not take place as we have described both parties.

Fig.3 Crashed vehicle Kia Rio [7]

Damage to the left side of the vehicle suggest Although the first part of the version described by operator the liquidation department of insurance as a course of the incident, but damage to the front of the car has not. The liquidator found that traces of damage to the vehicle is not in those places where they should be, if the accident occurred as both parties have described it. There would be on the left front bumper to its rupture and subsequent break and at the bottom which would damage the left front fog lights. The lower part of the bumper, however, showed no apparent damage. The bumper was damaged in the upper third and along with it the grille and bonnet.

In addition to the front of the bonnet at a height of about 40 cm above the ground was clearly visible horizontal dents which are in compliance collision with a truck, but this version does not match the description of the accident. This dents should certainly be situated on the left side of the engine hood and it would also mudguard. Based on the findings of fact and the liquidator decided to explore a truck Iveco Daily T. insured (the guilty). Damage to the vehicle Kia Rio was set to 62 000 CZK. [7] During the tour truck Iveco Daily T. see. Figure 4, the liquidator found that on the back of a truck insured there are no signs of damage, especially minor damage to the bumper and remnants of red paint after a collision with a vehicle Kia Rio.

Fig.4 The rear of the truck Iveco T. Daily [7]

In addition, the insured truck had approached in a completely different angle, which would turn him from without rear side of the cargo area of the vehicle caught Kia Rio. For if the truck ran into vehicles damaged as both participants consistently reported traffic accidents in the first part of the version it would certainly catch the back of a truck on a vehicle damaged at the level of the windows and doors the consequence of which would have been breaking windows and damaging the door pillar which has not happened. Furthermore adjuster found that the insured vehicle has on the rear side absolutely no traces of conflict which is not possible after such an accident. Certainly would crash after the vehicle has been damaged in minor damage to the rear of the truck and especially damage to the left rear lights, because they are at the height of the bumper of the vehicle Kia Rio.

Evaluation findings

Based on the fact to the insurance company concluded that the accident-damaged vehicles could meet and decided to ask for an expert opinion. Legal expert on the underlying materials and findings on a tour of a crashed car Kia Rio car and truck Iveco Daily T. unequivocally declare that this collision of vehicles [7]. On the basis of expert opinion was from the insurance company to deny payment of indemnity for damage event the vehicle Kia Rio and has filed a criminal complaint for attempted insurance fraud to the Police ČR [7].

Conclusion

Although insurance companies are more successful in detecting insurance fraud through the use of the latest technologies and ever more efficient methods of investigation of motor vehicles as seen on the described specific cases, the number of offenders in the coming years rising. Not only for the reason that there has been an increase in the statutory minimum amount of damage at which the police must be invited to an accident, but also in the context of long-lasting economic crisis.

References

- Konrád, Z. a kol.: Metodika vyšetřování jednotlivých druhů trestných činů. Praha: PA ČR, 1996.

- Zuzaňák, A.: Právní rádce pojištěných. Praha 1996. ISBN 80-7201-002-6

- Čejková, V. Řezáč, F. Šedová, J.: Pojišťovnictví – praktikum. Brno 1996. ISBN 80-210-1448-2

- Straus, J. a kol.: Kriminalistická technika. PA ČR, Praha 2005

- Porada, V a kol. Kriminalistika Akademické nakladatelství CERM,2001

- Chmelík, J. Porada, V.: Pojistné podvody. Praha: Policie ČR, 2000.

- CHROBÁK, Pavel. Specifika při vyšetřování podvodů s motorovými vozidly [online]. Zlín, 2010 [cit. 2014-22-7]. Diplomová práce. UTB Zlín. Dostupné:

http://dspace.k.utb.cz/handle/10563/11684 - Pojištění cz. Pojistné podvody [online]. 2014 [cit. 2014-07-11]. Dostupné z:

http://www.opojisteni.cz/pojistovny/cap/ - Česká asociace pojišťoven [online]. 2008 [cit. 2010-02-21]. Tiskové zprávy. Dostupné z:

http://www.cap.cz/images/tiskove-zpravy/2014-2-18-12-24.pdf